Small Businesses Applying for Loans Deserve and Need Transparent Pricing

Our goal is simple: pass the Small Business Financing Transparency Act (HB744 HA #1) in Illinois to require non-bank lenders to disclose APRs to small business borrowers. With transparency, entrepreneurs can make informed decisions, protect their employees and keep wealth in our communities.

Advocates call for IL small business loan transparency plan

$459M

lost every year by Illinois small businesses to predatory, out-of-state lenders charging sky-high rates without disclosing them2

200-400%

APR is common for loans marketed with “factor rates” or “specified percentages” — but borrowers are never told the actual APRs

APR is the missing link

Access our “APR Explained” fact sheet here.

Non-bank lenders often advertise their products using “factor rates,” “simple interest rates,” or “specified percentages,” or tell you to focus only on the “dollar cost.” These numbers sound simple — but they hide the true cost of borrowing.

Think of it this way: No one questions using “miles-per-hour” to understand the speed of a car, even if the person is only driving for thirty minutes. No matter how long you’re driving, you’re still going 60 miles per hour. Whether we’re talking about an hour or a year, the unit of time just enables you to make a comparison. Paying a 350% APR for 6 months is still expensive, just like driving 120 miles-per-hour for thirty minutes is still fast.

When it comes to loans the principle is the same. In order to make an apples-to-apples comparison, small business owners need to know the all-in price, over a common unit of time: the Annualized Percentage Rate.

APR is the gold standard. APR has been the legally required metric to make apples-to-apples comparisons between loans since the 1960s, and is supported for small business lending by Federal Reserve research.

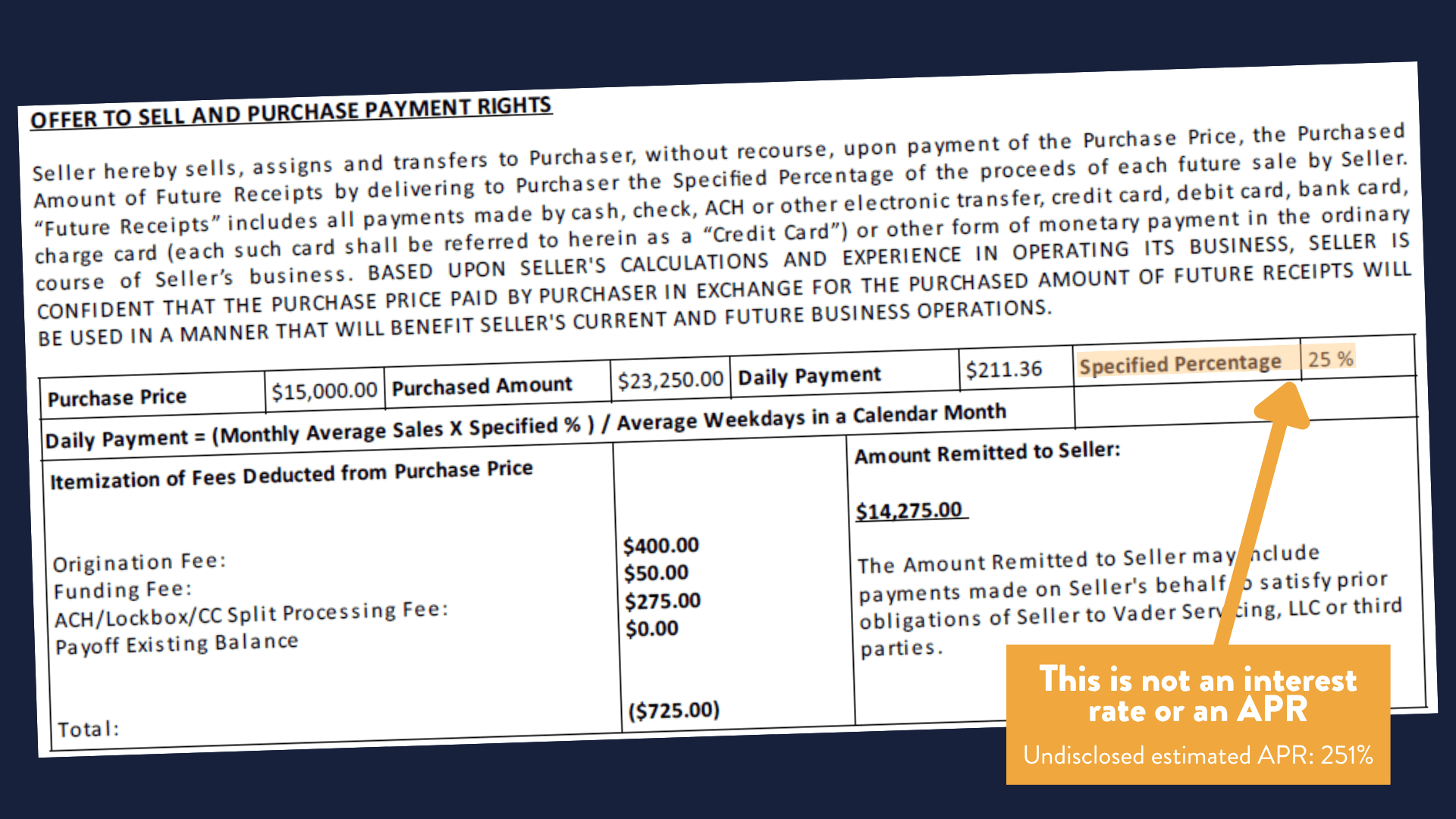

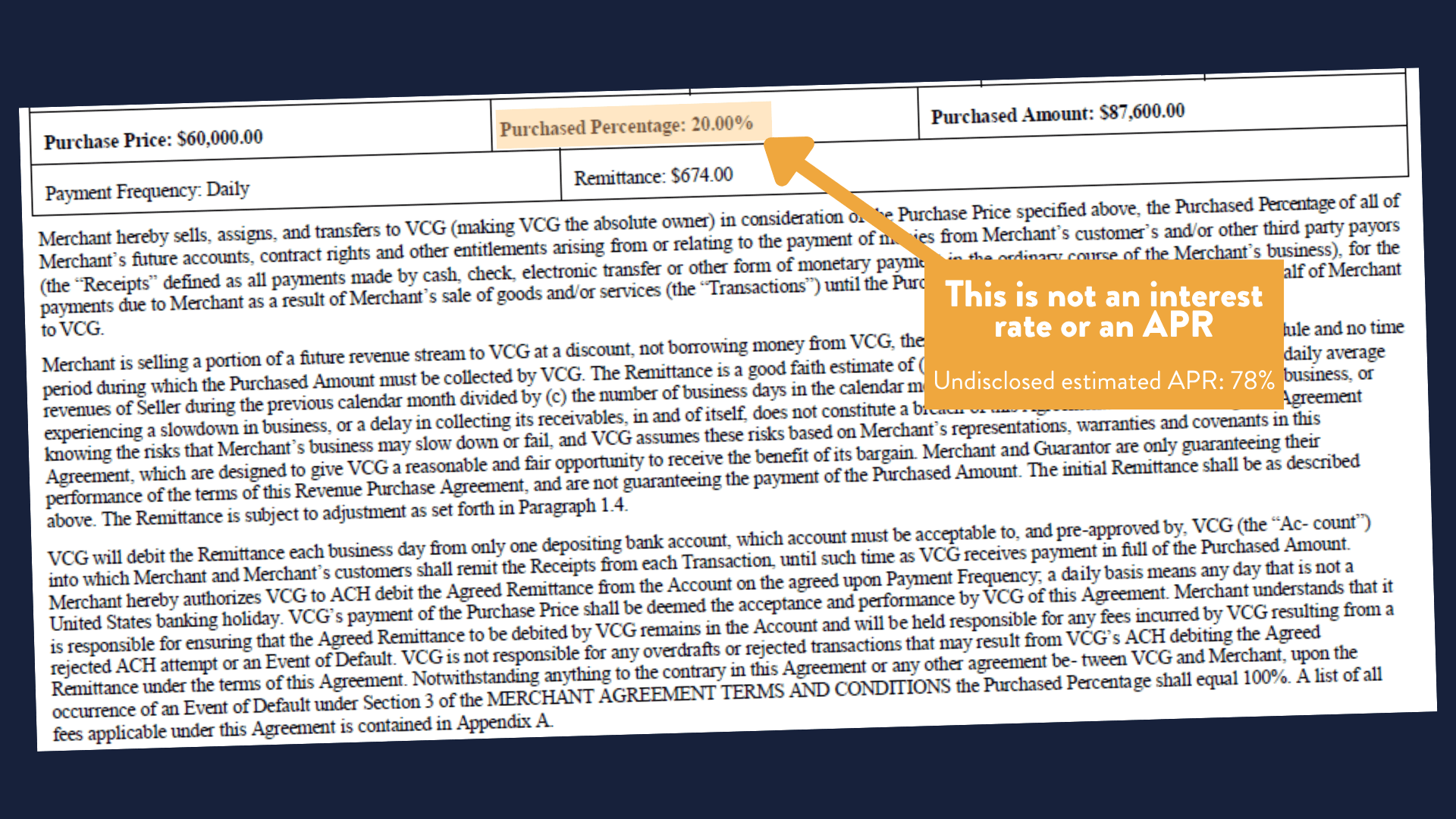

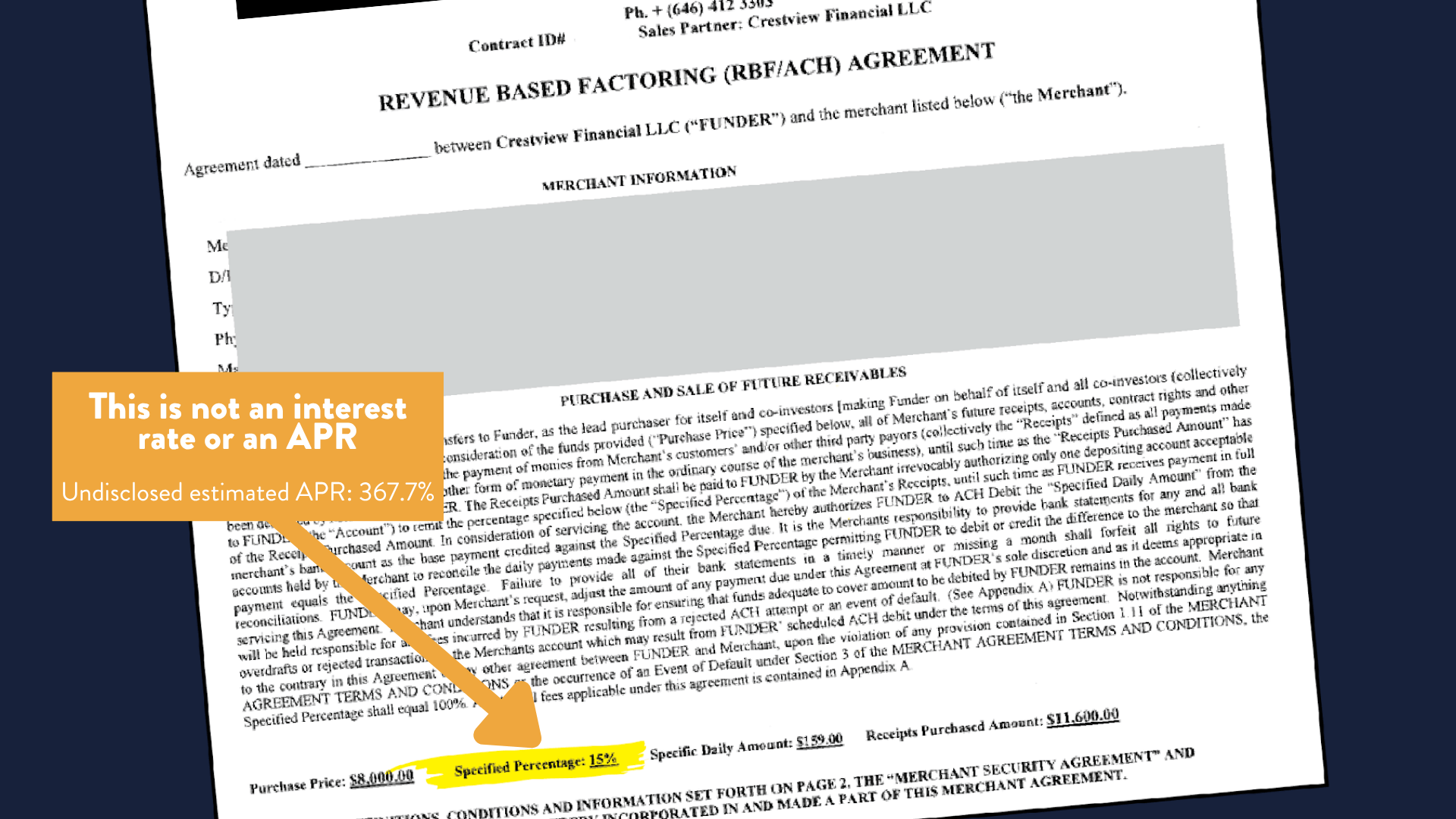

15% SPECIFICED PERCENTAGE

Total repayment amount: $11,600

Fees: $295 origination fee, $395 ACH fee, and $150 UCC termination fee

Term: 101 days

Daily payments

NOT DISCLOSED 367.7% APR5

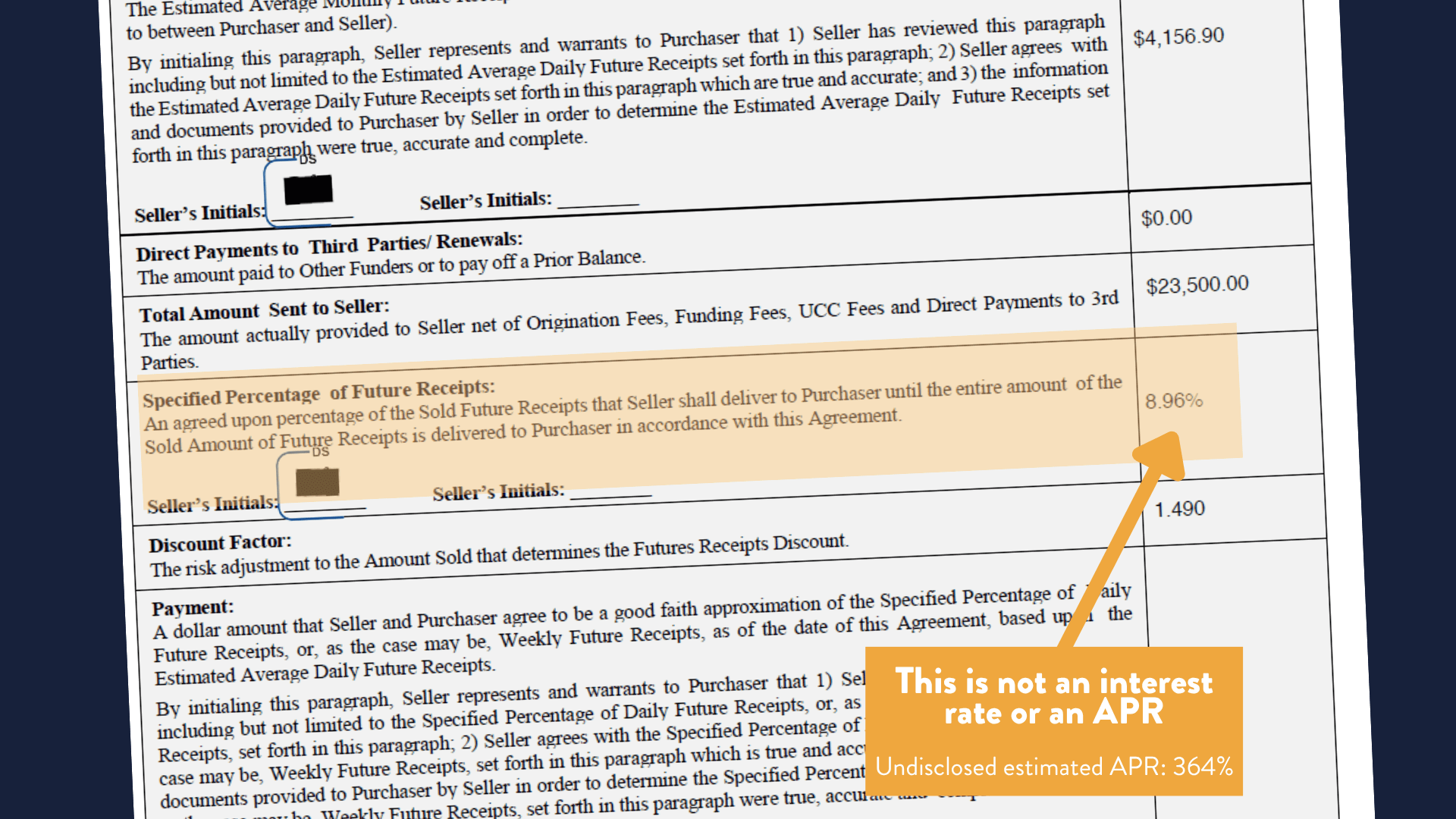

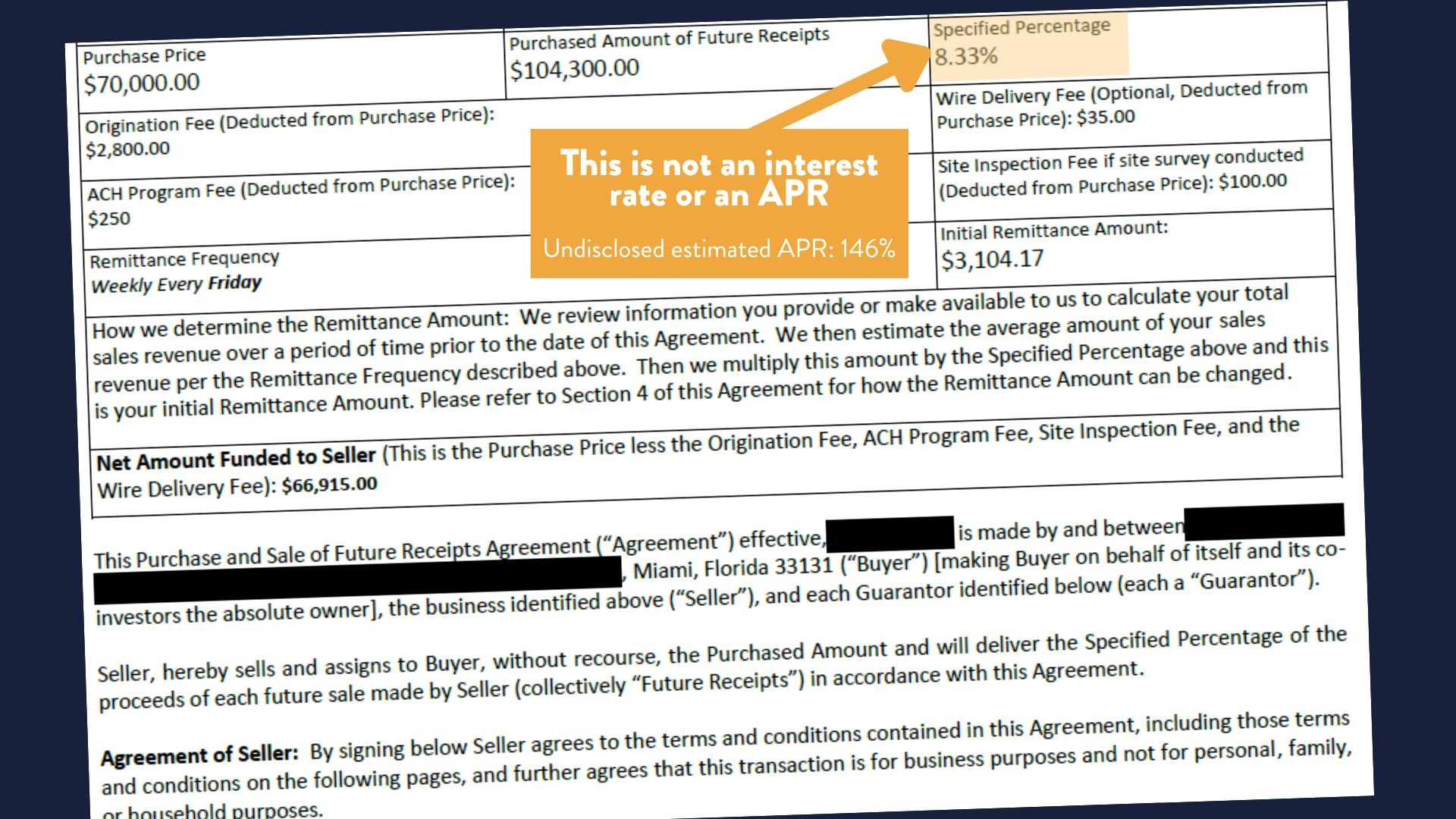

1.15 Factor Rate

Total repayment amount: $59,000

Fees: 2.5% set-up fee; $50/month administrative fee

Term: none (assume repaid in six months)

Daily payments (assume steady payments five days/week)

NOT DISCLOSED 70% APR6

4% Fee Rate

Total repayment amount: $56,500

Fee ate: 4% (months 1-2), 1.25% (months 3-6)

Fees: none

Monthly payments

Six-month term

NOT DISCLOSED 45% APR6

9% simple interest

Total repayment amount $54,500

Fees: 3% origination fee

Weekly payments

Six-month term

NOT DISCLOSED 46% APR6

Voices for Transparency

Join The Coalition

United for Transparent Lending

Executive Branch Endorsements

Local Elected Official Endorsements

Take Action For Transparent Lending

Small businesses deserve and need the same transparency as consumers. Together, we can close the loophole excluding small businesses from transparency, protect entrepreneurs, and keep wealth in Illinois communities. Add your voice and urge your lawmaker to act today.

Frequently Asked Questions

What is APR and why does it matter?

APR, or Annual Percentage Rate, shows the cost of a loan, including fees and interest, over the same period of time–the year. This helps people make an apples-to-apples price comparison between financing options. Without APR, small businesses are left comparing “factor rates” or other “rates” that Federal Reserve research shows confuse many borrowers.

Don’t small businesses know what they’re signing up for?

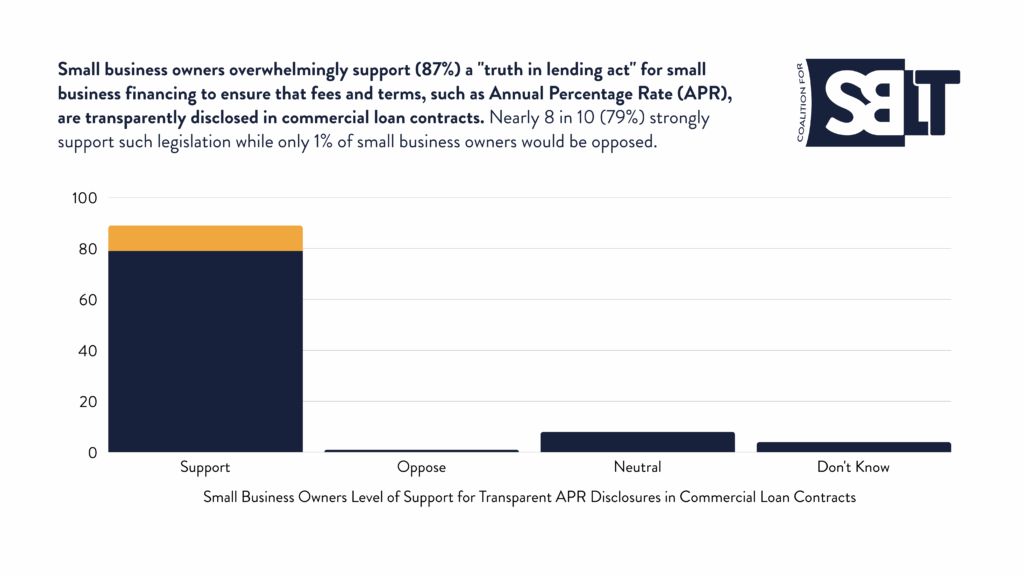

Polling from Small Business Majority7shows that small businesses overwhelmingly favor a “truth in lending act” for small business financing to ensure that fees and terms, such as APR, are transparently disclosed in commercial loan products.

Will this law limit access to capital?

Do other states already have this law?

Why is APR considered a critical part of transparency?

APR has been the keystone of price transparency in financing since the 1968 Truth in Lending Act. APR is just: what you pay, as a percentage of how much financing you get to use, over a common unit of time–the year.

You can think of APR as the “unit price” for financing. Back in 1967, Senator William Proxmire explained the importance of APR in Truth in Lending:

“Just as the consumer is told the price of gasoline per gallon, so must the buyer of credit be told the ‘unit price.’ Historically in our society that unit price for credit has been the annual rate of interest or finance charge applied to the unpaid balance of the debt.”

In fact, the Federal Reserve research calls financing products that do not disclose APRs, “higher-cost and less-transparent,” The Federal Reserve has published 5 studies showing that, in the absence of transparent APR disclosure, small business owners are being misled into unnecessarily expensive financing products. (2022, 2019, 2019, 2018, 2015)

These are some of the reasons why this bill is supported by small business groups, lenders, civil rights groups, and nearly everyone other than those pushing “higher-cost and less-transparent credit products,” to use the Federal Reserve’s words.

Shouldn't disclosing "total cost of capital" be enough?

Think of it this way: It would be like comparing job offers from two companies, where one tells you that you’ll be paid $5,000 per month, and the other tells you you’ll be paid $50,000 per year. $50,000 is a lot of money, so you’re inclined to take this job. But that would be a mistake because if you annualized the other job offer, it would pay $60,000 per year. APR helps you compare the dollar amount over the same period of time.

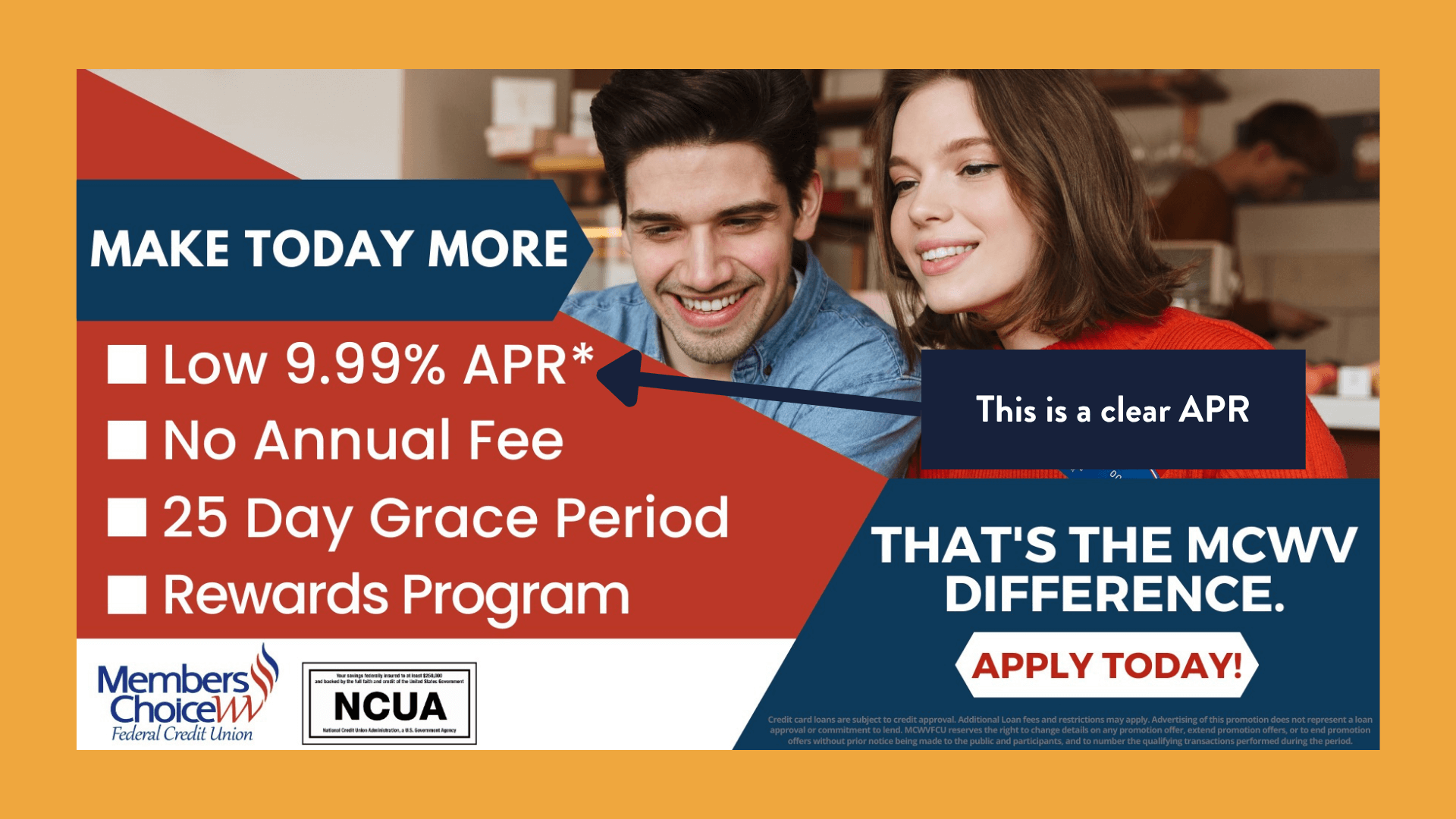

We expect to know the APRs of our car loan, our student loan, our credit cards, and our mortgage. Similarly, small business owners should be entitled to know the APR of the loans that are offered to them.

What about loans shorter than a year? Isn’t an annual rate inappropriate?

This question is meant to muddy the waters of an issue that is crystal clear. When we use “miles-per-hour,” it doesn’t matter whether you’re driving for less than an hour or more than an hour. You’re still going 60 miles per hour. Whether we’re talking about an hour or a year, the unit of time just enables you to make a comparison. Paying a 350% APR for 6 months is still expensive.

In The News

Transparency in lending practices protects small businesses

Column by Elliot Richardson

The push for transparency in small business loans

NPR Interview with Brian Mackey

Why Online Small Business Loans Are Being Compared To Subprime Mortgages

Forbes Article by Laurn Shin

Brokers Get Big Commissions for Selling Entrepreneurs Costly Loans

Bloomberg Article by Patrick Clark

Wall Street Finds New Subprime With 125% Business Loans

Bloomberg Article by Zeke Faux

Small businesses need loan transparency

Daily Herald Letter to the Editor by State Rep. Mary Beth Canty & State Senator Chris Belt

Advocates push “APR for All

Capitol City Now Article by Dave Dahl

The Predatory Lending Machine Crushing Small Business Across America

Bloomberg Article by Various Authors

An Easy Financing Source Pushes Some Small Businesses Into Bankruptcy

The Wall Street Journal Article by Becky Yerak

Shady Loans Are Bankrupting America's Small Businesses

Bloomberg Articles by Various Authors